28 of 2011 the TAAprescribing the rules related to. Changes that have been made appear in the content and are referenced with annotations.

Taxes Around The World Infographic Infographic Life Management Skills Global Education

Section 1032 is an anti-avoidance provision which essentially allows the Commissioner of the South African Revenue Service the Commissioner to disallow the setting off of an assessed loss or balance of an assessed loss against the companys income if.

. 1 The advance ruling pronounced by the Authority or the Appellate Authority under this Chapter shall be binding only. Act Nepal provides in depth comprehensive content with many tools summaries a forum for acts rules regulations in Nepal. B on the concerned officer.

For purposes of the preceding sentence the term tax-exempt IDB means any industrial development bond as defined in section 103b of the Internal Revenue Code of 1954 now 1986 the interest on which is exempt from tax under section 103a of such Code. An Interim Response 1. Certificate for tax deducted.

Tax Avoidance and Section 103. 1 Where a resident taxpayer derives foreign source income chargeable to tax under this Ordinance in respect of which the taxpayer has paid foreign income tax the taxpayer shall be allowed a tax credit of an amount equal to the lesser of. Permits licences and rights.

Lodging an objection or appeal against an assessment or decision. 2 For the. Section 103 2 can only apply if the relevant change in shareholding was entered into with the sole or main purpose of utilising an assessed loss to reduce or avoid tax.

Recovery from persons leaving Malaysia 105. In this regard the provisions of section 1032 of the Income Tax Act must be considered. Non-residents and part-year residents.

Section 1032 is an anti-avoidance provision which essentially allows the Commissioner of the South African Revenue Service the Commissioner to disallow the setting off of an assessed loss or balance of an assessed loss against the companys income if certain requirements are met. In terms of section 1034 of the Income Tax Act the taxpayer bears the onus of proving or showing that the relevant change in shareholding was not entered into with the sole or main purpose of. The Income Tax Act 103 of 1976 intends.

Tax Avoidance and Section 103 of the Income Tax Act 1962. B the Pakistan tax payable in respect of the income. Provisions supplementary to sections 101 and 102.

Section 1032 is an anti-avoidance provision which essentially allows the Commissioner of the South African Revenue Service the Commissioner to disallow the setting off of an assessed loss or balance of an assessed loss against the companys income if. Recovery by suit 107. Sole or main purpose.

For purposes of paragraph 1 average maturity shall be determined in accordance. In this regard. To fix the rates of norinal tax-payable by persons other than companies in respect or taxable incomes for the years of assessment ending on 28 February 1977 and 30 June 1977 and by companies in respect of taxable incorites for years of assessment ending dming the period of twelve.

1 Where sales of associated parcels of shares in a company being sales to the same person take place at different times and in consequence of any of the sales other than the first that person obtains control of the company then for the purposes of either of. Deduction of tax from emoluments and pensions 107 A. In this regard the provisions of section 1032 of the Income Tax Act must be considered.

Security for tax payable by withholding. Introduction The release of the Discussion Paper on Tax Avoidance and Section 103 of the Income Tax Act Discussion Paper on 3 November 2005 has sparked a high degree of interest and public comment1 The response moreover has generally been open and. PLR200646017 Tax Exempt Interest under Section.

Section 103 2 is an anti-avoidance provision which essentially allows the Commissioner of the South African Revenue Service the Commissioner to disallow the setting off of an assessed loss or balance of an assessed loss against the companys income. Payment of tax 103 A. 1 Every person deducting tax in accordance with the foregoing provisions of this Chapter shall within such period as may be prescribed from the time of credit or payment of the sum or as the case may be from the time of issue of a cheque or warrant for payment of any.

There are changes that may be brought into force at a future date. Income Tax Act 1967. Services for foreign nationals.

The word purpose is not defined in the Income Tax Act but is generally defined to be something set up as an object or end to be obtained refer. Applicability of advance ruling. Refusal of customs clearance in certain cases 106.

Section 203 of the Income Tax Act. This responds to a request for a ruling either that 1 Authority qualifies as a political subdivision for purposes of 103 of the Internal Revenue Code the Code or 2 the debt of Authority is issued on behalf of City within the meaning of 1103-1 b of the Income Tax Regulations. Section 103 of the CGST Act.

Deduction of tax from. Income Tax Act 2007 Section 103 is up to date with all changes known to be in force on or before 05 April 2022. Income Tax Act must be considered.

Income Tax Act 2058 2002. In this regard the provisions of section 103 2 of the Income Tax Act must be considered. 62 For the purpose of this section the income of a person who is non-resident at any time in a taxation year is deemed to be equal to the amount that would if the person were resident in Canada throughout the year be the persons income for the year.

550 published in the Gazette on 11 July 2014 new rules werepromulgated under section 103 of the Tax Administration Act No. A on the applicant who had sought it in respect of any matter referred to in sub-section 2 of section 97 for advance ruling. In terms of Government Notice No.

Operating Activities Section By Direct Method Accounting For Management Direct Method Method Activities

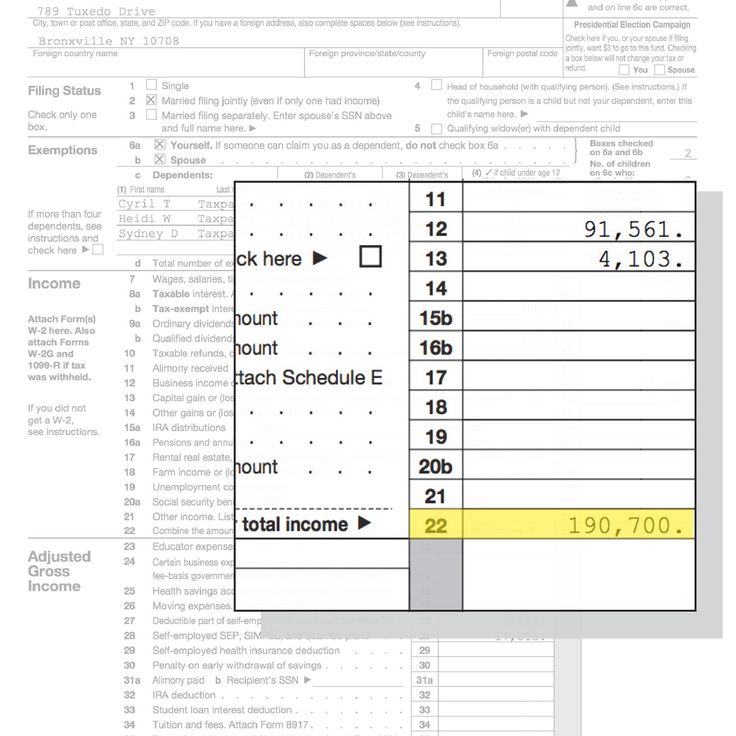

How To Fill Out Your Tax Return Like A Pro Published 2017 Tax Tax Return Tax Forms

Pin By The Taxtalk On Income Tax Deposit Accounting Cash

Tips For Business Record Keeping Paycheck Simple Math Paying

Do You Need Personal Business Loan At 3 If Yes Contact Us For More Info Email Farhanaziz Financehome Aol Com Business Loans Business Person 24 Hour Service

If Deduction Towards Expenses Is Not Denied Then The Liability Related To Such Expenses Can Not Be Treated As Unexplained Liability Deduction Income Tax Taxact

How To Fill Out Your Tax Return Like A Pro Published 2017 Tax Tax Return Tax Forms

Financial Literacy Word Wall Video Video Word Wall Financial Literacy Consumer Math

Latest News Chartered Accountant Insurance Industry Dividend

Taxupdate Taxlaw Tax Taxsaving Taxseason Taxrefund Taxreturn Incometaxseason Incometax Incometaxreturn Chart Income Tax Return Income Tax Tax Refund

Taxact Review Doing Your Own Taxes Made Easier Taxes In 2022 Taxact Online Taxes Personal Savings

Contact Form 1 Sarah Tax Services Tax Refund Tax Prep

General Ledger Account Numbers Chart Of Accounts Accounting Chart Of Accounts General Ledger

Pin On Taxation Guruji

Csa Related Donation Heal Subrahmanyam Pasumarty In 2022 Healing Charitable Contributions Taxact

Pin By Sue Wortman On Brain Candy Minimum Wage Wage Work Week

Infographic This Is What The Average Taxpayer In America Looks Like Infographic Infographic Inspiration Tax Refund

Filing Makes Expanding Your Business Easier In 2022 Income Tax Return Tax Return Income Tax

Understanding Your Law Firm S Financial Levers 2022 Lawyerist Law Firm Cash Flow Statement Legal Firm